A Historic Reversal, 29 Years in the Making

In the course of 2025, a symbolically important shift occurred in global central bank reserve composition. According to the European Central Bank, gold accounted for 27% of global central bank reserve assets at the end of 2025, surpassing US Treasury holdings (22%) for the first time since 1996. A year earlier, gold’s share stood at 20%, while Treasuries stood at 25% — meaning gold gained 7 percentage points while Treasuries lost 3. It is worth noting, however, that dollar-denominated assets as a whole (including deposits and other instruments beyond Treasuries) still made up the largest single category at 42% of total reserves.

This shift reflects two forces working together. The first is a pure price effect: gold crossed $4,000 per troy ounce for the first time in October 2025 and exceeded $5,500 in January 2026. The second is actual buying volume: central banks added a net 850 tonnes of gold in 2025. While this represented a slowdown from the 1,000-plus tonnes purchased annually in each of 2022, 2023, and 2024, it remained well above the 2010–2021 average of roughly 470 tonnes per year. The ECB reported that global central bank gold holdings now exceed 36,000 tonnes, approaching the roughly 38,000 tonnes held at the height of the Bretton Woods system.

This piece traces the institutional history behind this shift — from the 1971 Nixon Shock through five decades of competition between gold and the dollar for monetary primacy — and examines how recent developments in stablecoins and real-world-asset (RWA) tokenization connect to this longer arc.

The Nixon Shock and the Severing of Gold and the Dollar

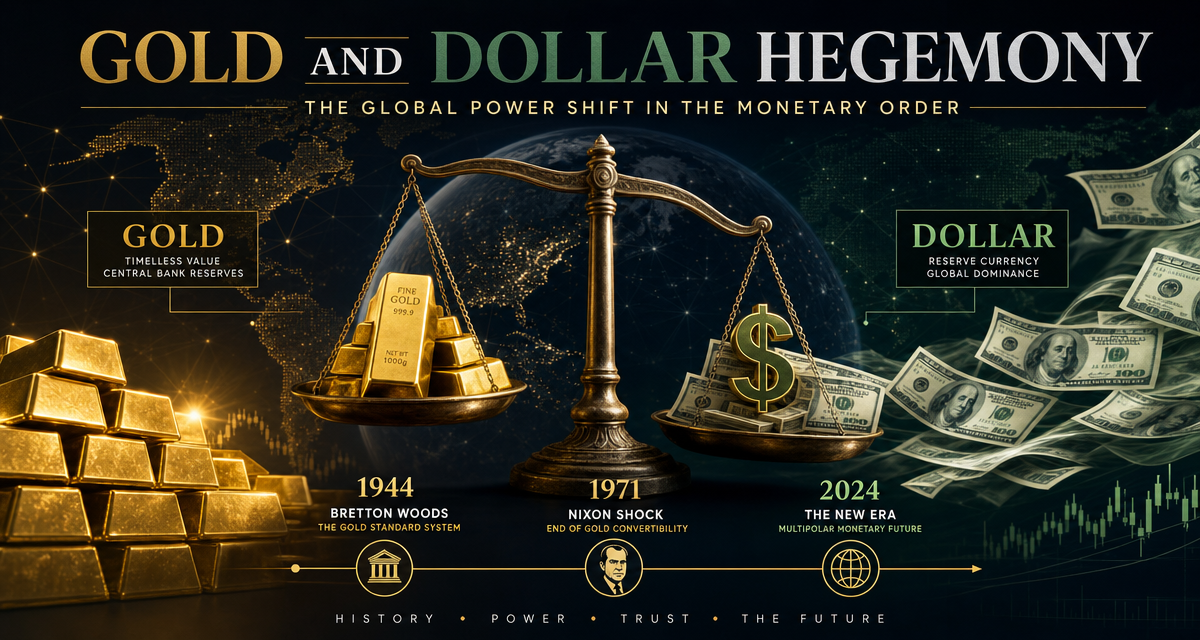

Under the 1944 Bretton Woods system, the dollar was pegged to gold at $35 per ounce, while other currencies were pegged to the dollar. Rising US spending through the 1960s, including Vietnam War expenditures, led to a buildup of dollars held abroad and growing pressure on the United States to redeem them in gold. Major economies operated a “Gold Pool” from the early 1960s, selling reserve gold into the market to keep its price stable, but this arrangement effectively collapsed in 1968 under surging demand. In August 1971, President Nixon suspended the dollar’s convertibility into gold — the so-called Nixon Shock — a move intended to give US monetary policy more flexibility, but one that also forced markets to confront a fundamental question: what, ultimately, counts as money?

Notably, official exchange-rate negotiations continued for several years after the shock. The December 1971 Smithsonian Agreement revalued gold to $38 per ounce, and a further adjustment to $42.22 followed in February 1973. However, the market price of gold had already decoupled sharply from these official figures, and attempts to maintain a fixed official rate ultimately failed. The 1976 Jamaica Accords, agreed by IMF members in Kingston, formally abolished the official link between gold and the dollar and moved major currencies to floating exchange rates — marking the definitive end of the Bretton Woods framework, even in name.

Institutional Mechanisms That Constrained Gold’s Price

Following the Kingston system, US policy is often described as having weakened gold’s monetary standing through two channels.

The first was the development of gold futures markets. Legalization of gold futures trading in the United States around 1974–1975 enabled large-scale “paper gold” trading through exchanges such as COMEX. As derivative markets — where exposure to gold’s price could be taken on without physical delivery — grew far larger than the physical market itself, some analysts argue that notional trading volume began to exert significant influence over spot price formation.

The second concerns gold’s regulatory and accounting status. It should be noted precisely that physical (allocated) gold held by banks was already assigned a 0% risk weight as Tier 1 capital under the original 1988 Basel I framework — a nuance that is often simplified or lost in popular accounts. What changed under Basel III’s liquidity coverage ratio (LCR) rules was different: gold was not formally designated a “High-Quality Liquid Asset” (HQLA), meaning it did not receive the same top-tier liquidity treatment as cash or government bonds. The London Bullion Market Association (LBMA) issued a 2025 statement explicitly refuting widely circulated claims that gold had been “reclassified as Tier 1 HQLA” under Basel III, calling this online information inaccurate. In short, the popular narrative around gold’s regulatory reclassification is often more dramatic — and less precise — than the underlying regulatory text supports.

What is clear, nonetheless, is that central bank gold buying accelerated markedly around the phased implementation of Basel III beginning in 2019. The World Gold Council has cited Basel III-related regulatory changes as one contributing factor behind the 2019 pickup in official purchases, and from 2022 through 2024 central banks bought more than 1,000 tonnes annually for three consecutive years — the strongest sustained buying on record.

The 2008 Financial Crisis and a Reallocation of Trust

The 2008 global financial crisis originated in subprime mortgage-backed derivatives such as collateralized debt obligations (CDOs) and spread into a broader crisis of confidence in the highly leveraged US financial system. Some analysts argue this episode prompted the international community to question, for the first time at scale, whether US Treasuries should automatically be treated as the world’s premier risk-free asset. In practice, central banks shifted from net sellers to net buyers of gold in the years following the crisis, with accumulation accelerating further after 2010.

2022: The Ukraine War and the Shock of Asset Freezes

Following Russia’s invasion of Ukraine in 2022, Western governments froze an estimated $300 billion in Russian central bank assets held abroad. This sent an unmistakable signal to reserve managers worldwide: dollar- and euro-denominated foreign assets can be frozen or seized as a matter of political decision during geopolitical conflict. Market analysts at firms including VanEck have identified this episode as one of the key catalysts behind the subsequent surge in official gold buying. Central banks purchased a net 1,082 tonnes of gold in 2022 alone — the largest annual total since the 1950s.

Against this backdrop, several countries have also worked to repatriate gold held abroad or upgrade it to higher international certification standards. Germany has previously repatriated portions of gold held at the Federal Reserve Bank of New York and elsewhere, and European countries including France are reported to be diversifying storage locations and upgrading certification to LBMA “Good Delivery” standards. That said, granular claims about specific tonnages moved in specific years are often difficult to verify against primary sources and should be treated as reported estimates rather than confirmed official figures.

Gold Reserves by Country (Early 2026)

According to World Gold Council and IMF International Financial Statistics (IFS) data, major sovereign gold holdings as of early 2026 stood at approximately:

- United States: ~8,133.5 tonnes (essentially unchanged for decades; roughly 69–76% of total reserves)

- Germany: ~3,350 tonnes

- Italy: ~2,452 tonnes

- France: ~2,437 tonnes

- Russia: ~2,311 tonnes

- China: officially ~2,313 tonnes (about 9% of reserves). Some analysts believe China’s actual holdings, including purchases routed through state entities and the Shanghai Gold Exchange, may be considerably higher, though this remains an estimate rather than confirmed official data.

- India: ~880 tonnes

- South Korea: ~104.4 tonnes (roughly the high-20s/low-30s in global rank; about 1–2% of reserves)

Combined, Germany, Italy, and France hold roughly 8,200 tonnes — comparable to the US total alone. These Western holdings are largely legacy positions accumulated during the Bretton Woods era and have remained broadly static. By contrast, the most active accumulators in recent years have been emerging-market central banks — China, India, Turkey, and Poland in particular. Poland’s holdings grew from roughly 103 tonnes in 2018 to more than 580 tonnes by early 2026, and the central bank formally adopted a 700-tonne target, with Governor Adam Glapiński explicitly citing Poland’s exposed position on NATO’s eastern flank as the rationale.

Recent Developments: Stablecoins, RWA Tokenization, and a New Dollar Circulation Model

Recent US legislation requiring stablecoin issuers to back their tokens with reserves such as US Treasuries (commonly referenced as the GENIUS Act) has fueled discussion of a new, more automated mechanism for generating dollar demand — one that some commentators compare to the petrodollar system but without its reliance on individual countries’ political discretion. Under the classical petrodollar arrangement, oil-exporting nations such as Saudi Arabia made a discretionary policy choice to reinvest dollar oil revenues into US Treasuries. The structure now being discussed would instead route demand automatically: as AI computing services or digital asset transactions settle through dollar-backed stablecoins, the reserves backing those stablecoins flow into Treasuries as a structural byproduct, independent of any single country’s strategic decision-making.

It is important to underscore that this remains a developing area of policy discussion rather than a fully implemented system. The extent to which RWA tokenization — extending collateral markets by tokenizing gold, Bitcoin, or other assets — will be implemented, and under what regulatory framework, is still being worked out. Given how quickly related legislation and administrative policy are evolving, readers should consult current official sources for the latest status.

Overall Assessment

Looking across five decades of competition between gold and the dollar, a few balanced conclusions emerge.

First, the rise in gold’s share of central bank reserves is a real, statistically confirmed phenomenon, driven by a combination of price appreciation and genuine increases in physical purchasing.

Second, the underlying drivers are multifaceted: responses to geopolitical risk (most clearly illustrated by the freezing of Russian central bank assets), a strategic push by emerging economies to reduce dependence on the dollar, and, to some degree, shifting regulatory and accounting treatment. That said, narratives linking gold buying directly to Basel III reclassification are sometimes exaggerated or imprecise in public discourse, making it important to consult primary sources such as the LBMA and the Bank for International Settlements directly.

Third, given that dollar-denominated assets still represent the single largest category of global reserves (around 42%), it would be premature to conclude that “de-dollarization” is imminent or that the dollar’s reserve-currency role is collapsing. The data to date is more consistent with gradual diversification and risk management than with a wholesale regime shift.

Fourth, the stablecoin- and RWA-based dollar circulation model now under discussion is an intriguing policy experiment, but much of it remains unproven in practice. Continued monitoring of relevant legislation and implementation will be necessary as this space evolves.

Investment Disclaimer: This article is provided for informational purposes only, based on publicly available statistics and reporting, and does not constitute investment advice or a recommendation to buy or sell any asset. Gold, currencies, and digital assets are subject to substantial price volatility, and past trends do not guarantee future returns. Investment decisions should be made based on your own judgment and risk tolerance, and consultation with a qualified financial professional is recommended where appropriate. Figures cited reflect publicly available data as of the time of writing and may be revised or superseded by subsequent reporting.

Key Sources: European Central Bank, World Gold Council (Gold Demand Trends, Central Bank Gold Reserves Survey), IMF International Financial Statistics, Bank for International Settlements (Basel III), London Bullion Market Association (LBMA)